Download

Abstract

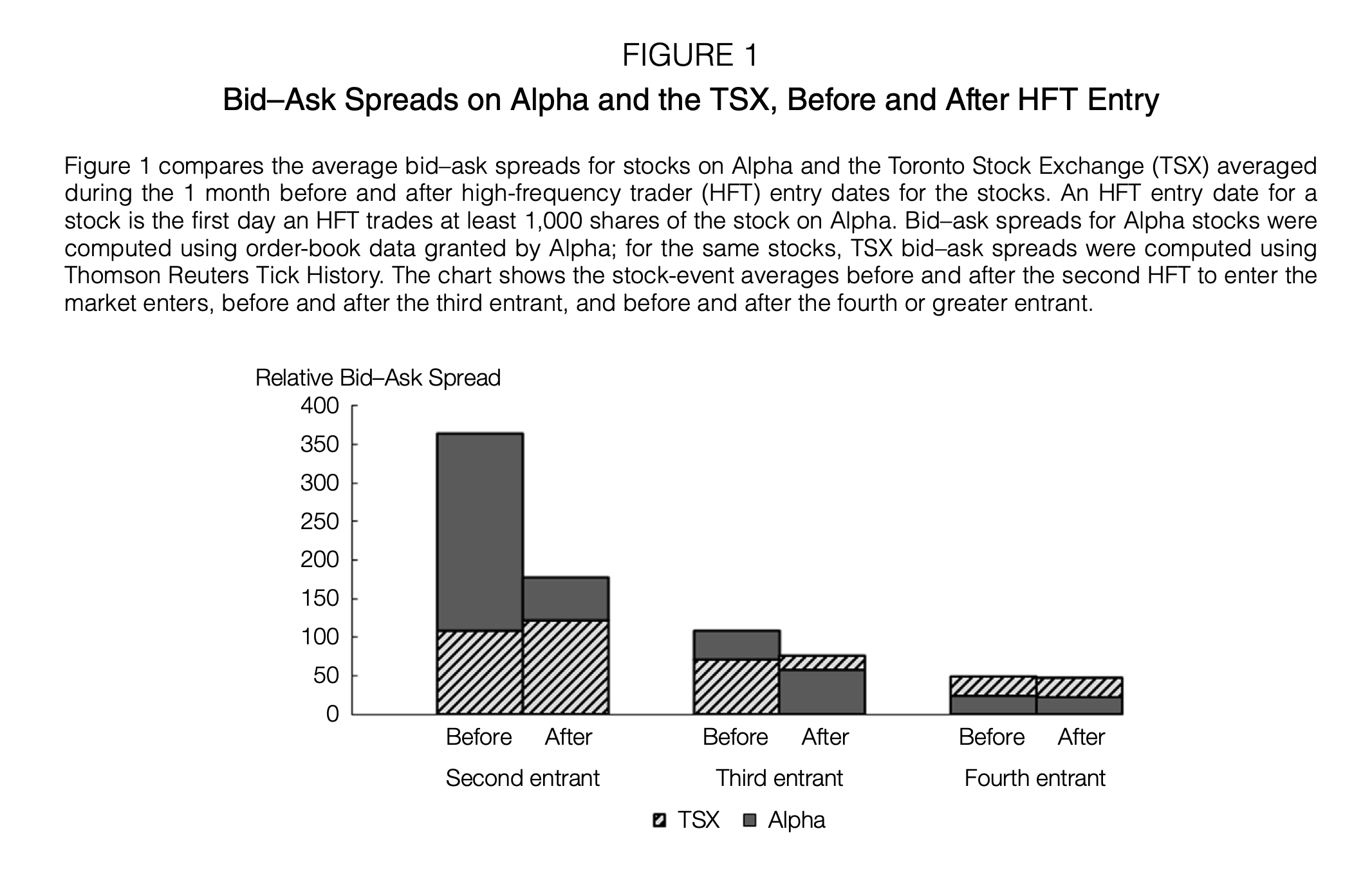

Theory on high-frequency traders (HFTs) predicts that market liquidity for a security decreases in the number of HFTs trading the security. We test this prediction by studying a new Canadian stock exchange, Alpha, that experienced the entry of 11 HFTs over 4 years. We find that bid–ask spreads on Alpha converge to those at the Toronto Stock Exchange as more HFTs trade on Alpha. Effective and realized spreads for non-HFTs improve as HFTs enter the market. To explain the contrast with theory, which models the HFT as a price competitor, we provide evidence more consistent with HFTs fitting a quantity-competitor framework.

Figure 1: Bid-ask spreads on the experimental exchange and the control exchange, before and after HFT entry

Citation

Brogaard, J., & Garriott, C. (2019). High-frequency trading competition. Journal of Financial and Quantitative Analysis, 54(4), 1469-1497.

@article{brogaard2019high,

title={High-frequency trading competition},

author={Brogaard, Jonathan and Garriott, Corey},

journal={Journal of Financial and Quantitative Analysis},

volume={54},

number={4},

pages={1469--1497},

year={2019},

publisher={Cambridge University Press}

}