Download

Abstract

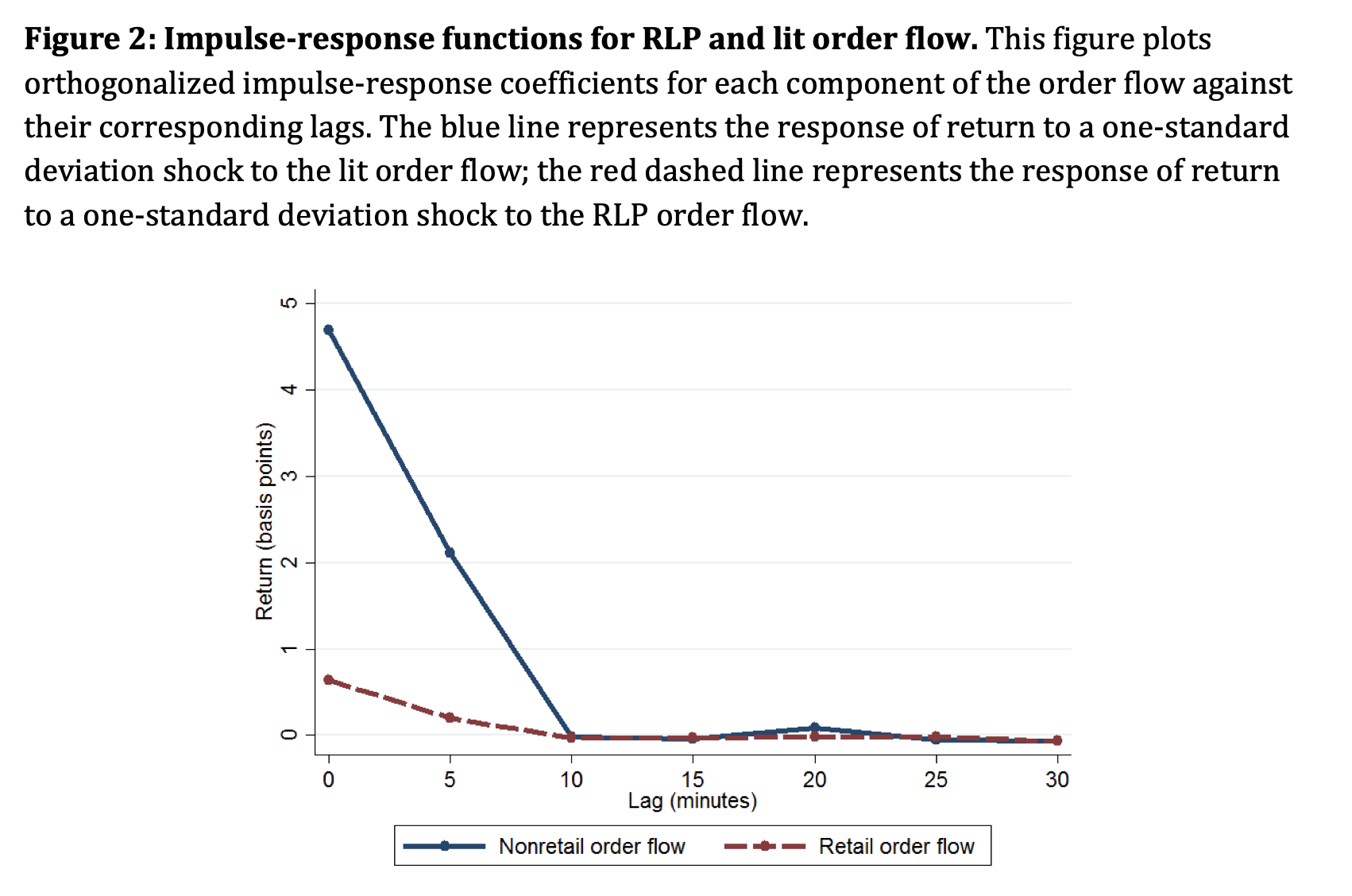

In August 2012, the New York Stock Exchange launched the Retail Liquidity Program (RLP), a trading facility that enables participating organizations to quote dark limit orders executable only by retail traders. A Hasbrouck (1991) structural vector autoregression shows that the facility increased the information content of the order flow by distinguishing retail trades from relatively more informed trades. A differences-in- differences event study finds that the RLP launch impacted market quality. Stocks with substantial RLP activity experienced mildly improved relative bid-ask spreads, effective spreads, price impacts and return autocorrelations in both the RLP and non-RLP segments.

Figure 2: The low price impact of retail trades on NYSE’s RLP compared to the main order flow

Citation

Garriott, C., & Walton, A. (2018). Retail order flow segmentation. The Journal of Trading, 13(3), 13–23.

@article{garriott2018retail,

title={Retail order flow segmentation},

author={Garriott, Corey and Walton, Adrian},

journal={The Journal of Trading},

volume={13},

number={3},

pages={13--23},

year={2018},

doi={10.3905/jot.2018.13.3.013}

}